Raghu Das, CEO, IDTechEx

The printed electronics equipment and consumables supplier base consists of over 100 global organizations, according to IDTechex Research in their report "Printing Equipment for Printed Electronics 2015-2025". The majority of these are based in Europe, followed by a roughly even share of US and Asian based companies. Within Europe itself, Germany is home to more equipment makers than other European countries.

Click iamge to enlarge

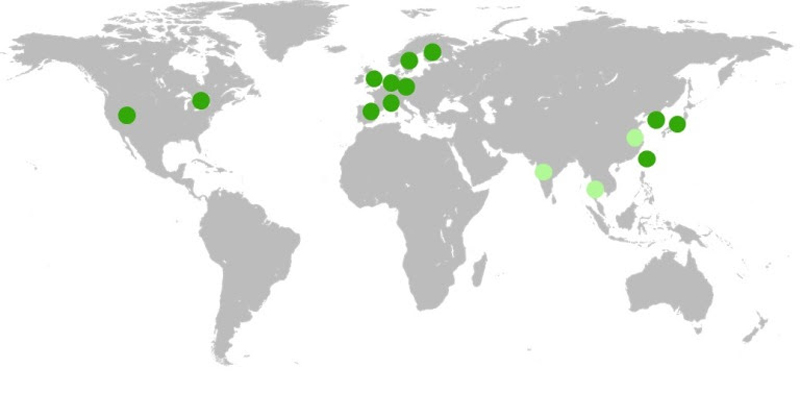

Printed electronics centers

While initially the printed, organic and flexible electronics industry was driven by significant investment and technological development from the fine chemicals industry, the equipment sector followed soon after. Those involved in screen printing and screen printing consumables have had the largest market so far in printed electronics given that the equipment is used in commercial products such as solar cells and glucose test strips.

For more emerging printed electronics processes, such as inkjet printing, specialist coating systems applied to printed electronics, gravure and flexo, the market has been smaller but quickly growing. Most of the sales of such systems have been into Europe. This has been due to a high and consistent level of funding made available from European funding sources in addition to country specific funding programs.

Printed electronics is in most European countries a relatively high prioritization category for funding. Many of the funding sources have found that one of the most useful things to kick start the industry in Europe would be to make equipment available so that people can develop, prototype, pilot and even make low quantity product without the need for them to buy their own equipment which is capital intensive and high risk as development still has to occur.

As a result, many printed electronics centers have been set up, as shown in the image below. Those in light green are in the process of being set up, darker green are more established centers. Some represent numerous centers.

Europe government funding for equipment declines

However, through many interviews IDTechEx Research has found that the equipment demand has mostly been met for the government funded programs. Of course, outside the government funded projects companies are buying equipment but the main funding until now has come from governments. For equipment supply companies, many of whom have enjoyed a good profitable period with top line sales growth, there is now a void as European companies' appetite for equipment lags the government funded programs.

The US equipment market has seen steady growth but until now has not been as big market as it is in Europe, due to lesser government funding. This has changed due to the recently announced $75 million funding for a printed electronics manufacturing hub, but this is one project unlike the European market which consisted of many.

Now, therefore, equipment makers are turning to Asia. There is an impending transition from equipment for development and prototyping purposes to buying equipment for higher volume manufacture. Here the equipment focus is different - it is not making state of the art transistors using printing, but doing simpler things but reliably that can be in commercial products today. For example, this includes using inkjet printers for the polymer planarization layers for barriers on OLEDs or printing the bezel edge electrodes for touch screens, often which are then patterned with a laser.

So now the wave of new printed electronics capability truly becomes applied to product, with equipment companies sending their sales people out to Asia.

The IDTechEx research report "Printing Equipment for Printed Electronics 2015-2025" assesses the applications, technologies and opportunities for equipment that is enabling printed electronics including looking at the main government centers and geographic trends. It covers the different types of printing, curing/sintering and other key manufacturing equipment, providing assessment of the manufacturing requirements for different applications, growth areas, ten year forecasts for each printing method by application and detailed company assessments.

PDF

PDF