Fueling the EV Boom: Will Copper Supply Meet Demand?

Electric Vehicle Market Growth and Insights into Its Impacts on Copper Demand.

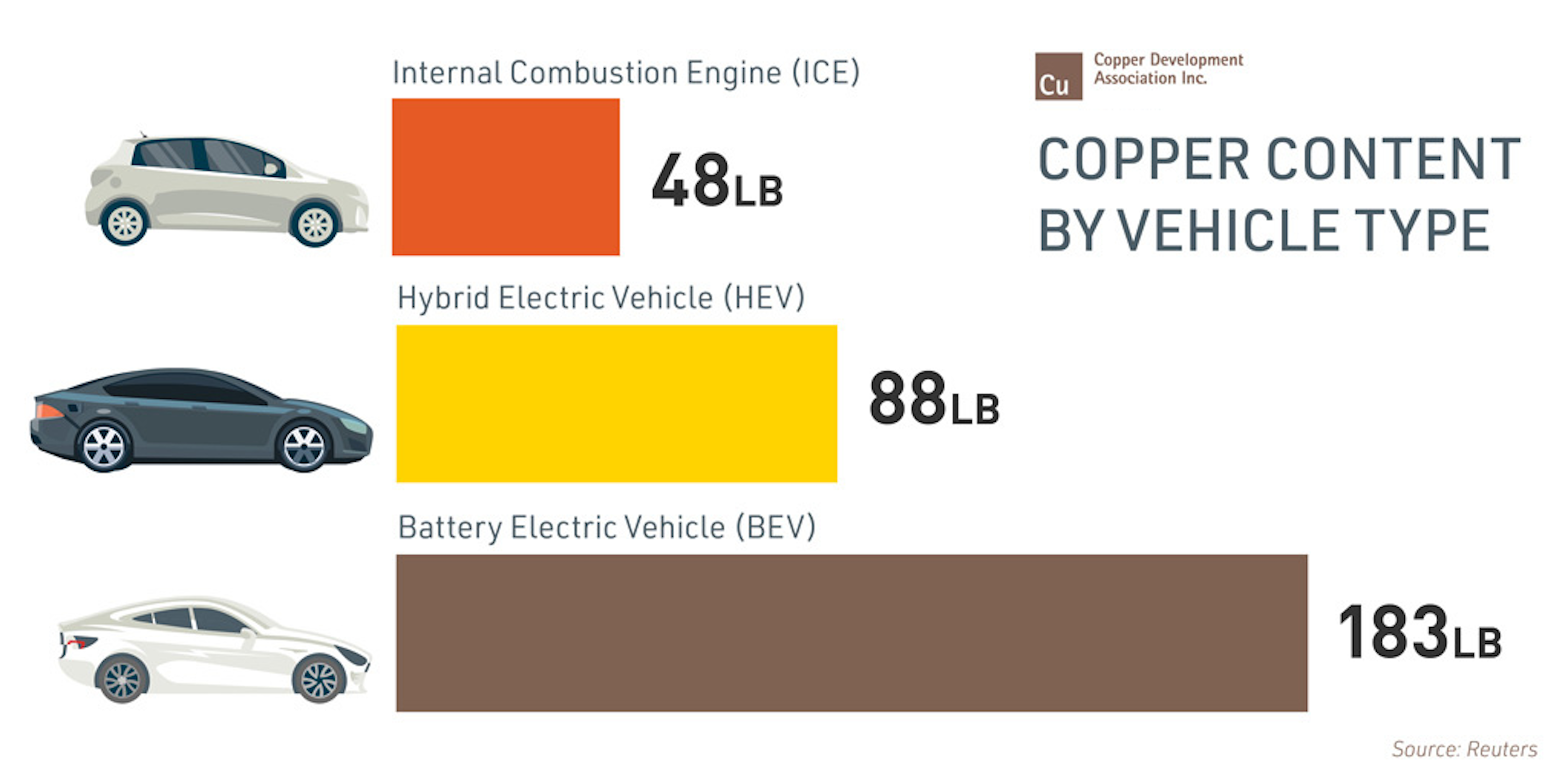

Figure 1: Copper Content by Vehicle Type: Comparing the Copper Usage in Internal Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and Battery Electric Vehicle (BEV) Vehicles

The transition to electric vehicles (EV) is widely seen as a crucial step toward achieving a net-zero emissions economy by 2050 in the United States. However, this shift has raised concerns about the availability of key raw materials, such as copper, to support the growing demand in the EV market. As governments and automakers set ambitious targets for EV adoption, the copper industry is questioned about a stable and sufficient supply to meet the predicted demand.

Copper in EVs and Why It’s a Preferred Material

While copper requirements for electric vehicles can vary depending on the specific model and type of EV (see Figure 1), it is extensively used in the wiring harness, which connects hundreds of components requiring power, control, or communication. Small motors that power various luxury features, such as windshield wipers, electric windows, and seat adjustments, also contain copper. While each of these motors may use only a small amount, a typical vehicle can collectively house over 20 such motors, further contributing to the significant copper content in EVs.

The EV battery itself contains a substantial amount of copper, with 92% in the form of copper foil within the battery cells and the remaining 8% used in the battery pack as busbars, cables, and wiring. Additionally, power electronics components, including the inverter, onboard charger, and DC-to-DC converter, incorporate copper in various parts. These include printed circuit boards, power modules, and internal cabling, ensuring efficient power management and distribution within the vehicle.

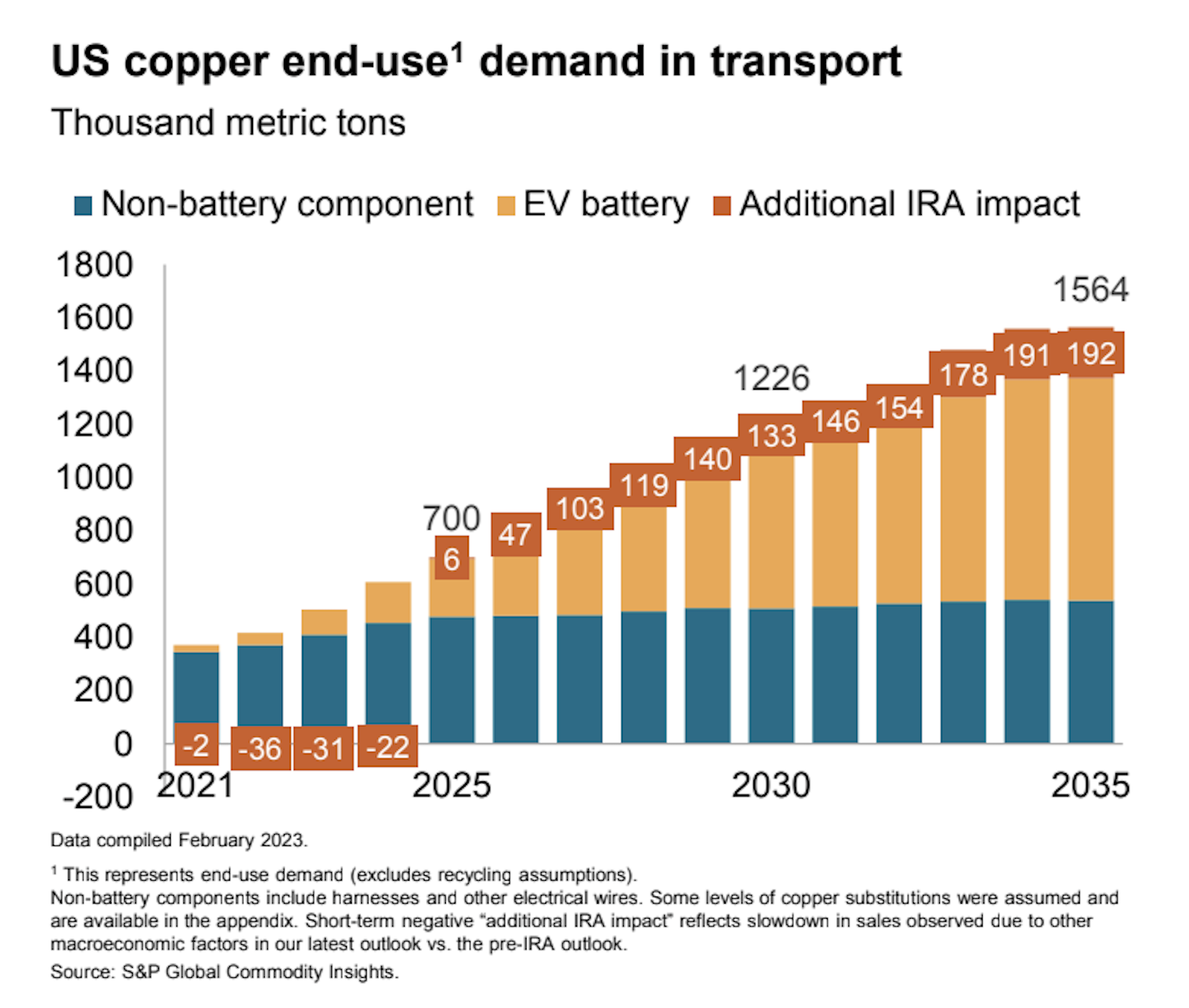

According to a 2023 S&P Global report titled "Inflation Reduction Act: Impact on North America Metals and Minerals Market," copper demand for electric vehicle (EV) batteries is expected to increase to roughly 1.2 million tonnes by 2035. To meet this growing demand driven by rising EV production in the United States, the auto industry will need to find sufficient quality sources to keep up with the surging need for copper (see Figure 2).

The cabling and infrastructure of EV charging stations are another source of copper usage. For example, BYD charging ports ranging from 3.3 kW (kilowatts) to 200 kW contain 2 to 17 pounds of copper each. Within the next decade, a network of five million charging ports will be needed to power the U.S.'s EVs.

Copper is preferred for various applications due to its exceptional conductivity, surpassing that of all other readily available metals for a given space. This high conductivity level (in as small of a package as possible) makes it an ideal choice, as copper provides superior performance without the prohibitive costs of alternative options.

Click image to enlarge

Figure 2: Projected Growth in US Copper Demand for Transport Sector: Accounting for Battery Electric Vehicles and Other Non-Battery Components

Beyond its superior electrical properties, copper boasts several other advantages. It does not corrode easily, is relatively strong compared to other metals, and it is malleable. These combined attributes make it the optimal choice, as substitutes would likely take up more space and lack similar functionality. EV manufacturers are actively exploring ways to improve the energy efficiency of their designs, recognizing the need to maximize performance while minimizing the physical footprint.

Meeting The Demand

The United States is well-positioned to address the rising demand for copper due to its own reserves and resources of 275 million metric tons of copper — more than enough to accommodate the peak clean energy demand through 2035. Supplementing these resources is a growing recycling industry encompassing pre-consumer and post-consumer efforts as well as imports from reliable trade partners. With all these efforts, we can collectively meet the future demand.

At the forefront, the Copper Development Association (CDA) is pushing for policy change in the United States to increase the domestic production of copper, both mining and refining. Permitting, among other hurdles, has left domestic copper production at a halt. Without new domestic production and refining, U.S. net imports of refined copper are forecasted to skyrocket to over 60%.

The policy changes advocated by the CDA, such as including copper on the U.S. Geological Survey’s Critical Minerals list, would unlock new opportunities across the domestic supply chain. The United States currently lacks sufficient copper refining and smelting capacity. The number of domestic refineries declined from nine in 2000 to five in 2023, resulting in a 40% drop in refined copper production.

To address this deficit, the United States must either expand its mining and refining facilities — a course of action most efficiently achieved through supportive policy change and incentives — or continue exporting its domestically mined copper ore for processing elsewhere.

Technological Innovations and Efficiency

EV production continues to grow, though predicting its trajectory remains challenging. It will largely rely on the ongoing decline of battery pack prices, the most significant cost component. As EV battery technology advances and these prices continue to fall, not only will the range of EVs produced increase, but we will likely come to an inflection point where the economic benefits of electric vehicles over gas-powered alternatives become undeniable. This, in turn, will trigger a significant surge in EV uptake.

Car manufacturers continually work to optimize their designs and minimize the use of raw materials, such as copper, as their models evolve. A key trend is moving toward modularizing electrical systems, creating zonal architectures where components are grouped into simpler interconnected modules (see Figure 3). This approach is expected to help drive further innovations in EV technology as the industry continues to advance.

Recycling

Copper recycling is becoming increasingly important in the electric vehicle market as EV adoption rises. However, compared with more established recycling streams, the supporting infrastructure and processes remain relatively underdeveloped. Enhancing the efficiency and scalability of methods to recapture copper from end-of-life, or post-consumer, EV components will be crucial for long-term sustainability.

Pre-consumer recycling encompasses all the scrap material recovered during the manufacturing process. This includes leftover parts and offcuts from processes like stamping. This scrap can then be recycled to recoup value and improve the overall efficiency of the business.

The post-consumer recycling of copper and other materials is an area with significant room for improvement in the United States. Once EV products are at the end of their useful lives, getting consumers to return the materials for recycling remains a challenge. There have been discussions about government support for recycling programs to help facilitate this process. However, it is acknowledged that many post-consumer products are shipped overseas for disassembly and recycling rather than being processed domestically, as it requires significant labor and is more economical elsewhere.

Copper-incorporating products tend to have remarkably long lifespans. Historically, a significant portion of all the copper mined remains in circulation, with little ending up in landfills. While the recyclability of copper is a positive attribute, the extended life cycles of these applications mean that recycling alone will not adequately meet the rising demand, particularly when driven by the growth of EVs.

Click image to enlarge

Figure 3: Copper busbars overlapping and fixed on EV onboard charger

Balancing Copper Supply and Demand

CDA is aware of the impending increase in copper demand driven by growing EV product applications. As a result, the association has been advocating for policy changes to boost domestic copper production. This is a response to declining domestic supplies and increased reliance on imports in recent years.

Limitations on domestic copper production and recycling have already increased the dependence on imports of refined copper, which has grown from 29.6% of the total copper supply in 2016 to 45.7% in 2023. The United States is currently the fifth largest copper-producing nation and has substantial untapped copper reserves that can be accessed, potentially through expanding existing mines, to help offset the need for greater imports.

The United States currently imports copper primarily from friendly, free-trade partners like Canada, Mexico, Peru, and Chile. Expanding supply chains to less familiar regions without established trade agreements poses challenges, though the good news is that copper resources are globally diversified.

Securing Copper Supply for the EV Future

Addressing the rising copper demand driven by the EV transition will require supportive government policies incentivizing domestic copper production, refining, and recycling, which can unlock new supply chain opportunities. Enhancing the efficiency and scalability of EV component recycling, pre- and post-consumer, will be crucial to long-term sustainability.

Fortunately, copper is well-suited to meet the needs of the EV industry. It is an abundant, highly conductive, and highly recyclable material, making it the optimal choice to power the vehicles of the future. Through a combination of policy support, technological innovation, and collaborative problem-solving, the copper industry can meet the increasing demands of the EV revolution and advance the transition to a sustainable, net-zero future.

.jpeg)